In the financial world it is important to be moneywise and understand how to make money work for you. It is necessary to stay informed about finances, as in today’s world interest rates and financial conditions change all the time. Sometimes, if you change the way you manage your loans can make a big difference in your long-term savings.

One of the most effective ways to make smart financial decisions is by learning more about finances and its strategies that help you manage your money wisely. Our blog’s main purpose is to educate people on their way to make smart financial decisions, and today’s topic is about how to refinance loans and save money.

This article is especially for you if you took out a loan a few years ago and recently noticed that banks now give much lower interest rates.

What is loan refinancing: how it works?

First thing first, let’s understand what is loan refinancing and how it functions.

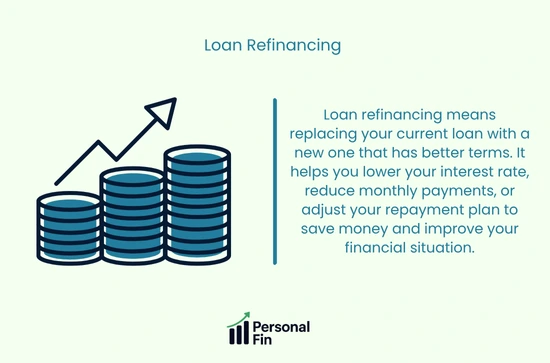

Loan refinancing is a financial strategy when people replace their existing loan with a new one which purpose is to make it easier to pay back, lower the interest rate, and save money in the long run. This is a very reasonable move because it eases the burden of your loan.

People usually refinance loans when interest rates drop, their credit score improves, or they want to change the length of their loan. Refinancing loan is an easy process and does not take much time. You simply need to apply for a new loan, use that money to pay off your old one, and then you can continue making payments on the new loan with a lower interest rate.

Types of loan refinancing

Let’s understand what types of loan refinancing there are because you can refinance many types of loans, not just one kind. You can refinance different kinds of loans in order to get better terms or lower your payments based on your financial goals.

Check out the 4 common types of loan refinancing:

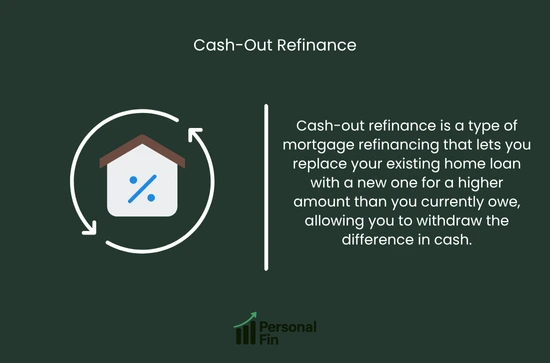

Mortgage Loan Refinance – The concept of this type of loan is the following: to replace the current mortgage with a new one in terms of lower interest rates. The majority of borrowers restructure their loans because they want to benefit from reduced interest rates, switch from an adjustable to a fixed rate or unlock equity through a cash-out refinance.

Auto Loan Refinance – The auto loan refinance consists of obtaining a new car loan which is used to pay off your previous auto loan. This can be seen as a strategic move if your credit profile has improved or if market rates have declined. In this situation borrowers may reduce their interest expenses and improve overall cash flow through lower monthly payments.

Student Loan Refinance – This type of loan refinance is profitable for students as they can combine their multiple loans into one loan, so they will only have one monthly payment with a lower annual percentage rate (APR).

Personal Loan Refinance – Personal loan refinance offers great versatility and you can apply it toward almost any purpose you prefer. Many individuals use them to handle urgent financial needs, significant life events such as weddings or property renovation projects. Personal loans are not backed by collateral, which means they don’t require any form of guarantee or asset as security. They may feature fixed or adjustable interest rates with repayment durations which range from several months to multiple years.

Top reasons to refinance loans

When you make a financial move it is crucial to know why you are doing it and how you will benefit from it in the long run. Refinancing a loan can be very beneficial depending on your financial status, situation and the terms of your new loan.

The main reasons to refinance loans are the followings:

- Receiving new loan terms: New loan terms mean different interest rate, new repayment period (for example, 3 years instead of 5), and a changed monthly payment amount.

- Reducing your interest rate: When you refinance a loan and get a lower interest rate you pay less money in interest over time. Even a small drop in interest rate can save you hundreds or even thousands of dollars depending on the size and length of your loan.

- Changing loan types: This means that when you change loan types you switch between different kinds of interest structures and most commonly from an adjustable-rate loan to a fixed-rate loan. A fixed-rate loan keeps an identical interest rate for the loan, and adjustable-rate loan starts with a lower interest and may change over time depending on market conditions.

- Consolidating debt: The main idea behind debt consolidation is simplicity because it allows you to combine several loans into a single one which often comes with a lower interest rate.

How to refinance loans step-by-step

In the beginning, the idea of refinancing may seem time-consuming and a bit complicated but after reading this step-by-step guide you’ll feel more confident and ready to refinance your loans for better financial management. Here’s a clear step-by-step walkthrough to help you through it:

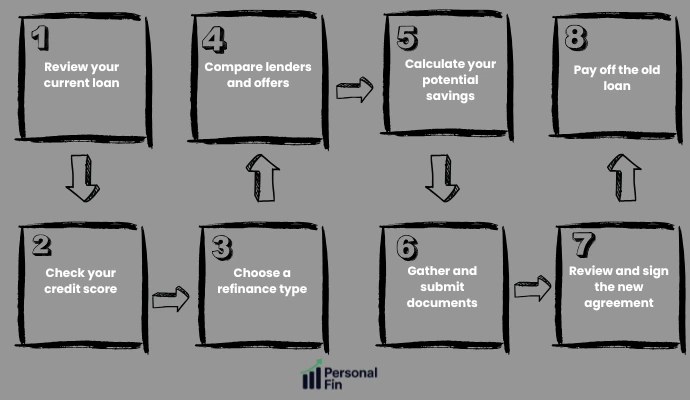

1. Review your current loan: First and foremost you must look at what you would like to change in your existing loan, such as high interest rate, or your current lender.

2. Check your credit score: Before you decide to refinance your loan take a closer look at your credit score as it determines whether you will get a new loan with a lower interest rate or not.

3. Choose a refinance type: With the third step you should choose the appropriate refinance type.

4. Compare lenders and offers: As you want to change your existing loan conditions and make them better you need to take your time and compare different lenders, see what they offer, choose the best repayment terms and find the most favorable deal for your situation.

5. Calculate your potential savings: There are many online loan refinancing calculators that will ease the burden of doing it by yourself and estimating how much you can save.

6. Gather and submit required documents: In this stage you need to prepare all necessary paperwork such as proof of income, credit history and identification. Make sure that you hand in complete and accurate documents that can speed up the approval process.

7. Review and sign the new agreement: During this phase you will need to carefully read through the new loan contract before signing it and make sure you understand the new terms.

8. Pay off the old loan: Lastly, once your get your new loan, pay off the previous one.

Common Mistakes to Avoid When Refinancing

As you already understand the financial world is very tricky and it is important to know what are the common mistakes that people make in case you want to avoid from making those mistakes too.

1. Not comparing multiple lenders: Many people who are not financially aware settle for the first lender they find and take their offer for granted. This is a typical mistake that most people make.

2. Ignoring fees and hidden costs: Another common mistake is ignoring fees and hidden costs which can significantly reduce or even eliminate the financial benefits of refinancing.

3. Extending your loan too much: We are already convinced that refinancing is mostly beneficial, however, stretching your loan term too far may increase the total interest you pay over time.

4. Refinancing with a low credit score: If your credit score hasn’t improved since your original loan, you may not be eligible for improved terms. Refinancing under those conditions may not bring any real financial benefit.

5. Not reading the new agreement carefully: The last common mistake is signing new contracts too quickly without reading the terms.

Should you refinance? Key considerations

Refinancing loans can be a smart financial move but only if you take the following key points into consideration, otherwise it will be a waste of time:

- interest rates (if the difference is small, it might not be worth it.),

- loan term,

- fees (remember to check for closing costs and additional charges, as they can reduce your savings),

- credit score (if your score has improved, refinancing might work in your favor.),

- and, financial goals.

Each of these above mentioned factors can have a big impact on your savings and financial stability.

Final Thoughts: Make Smart Financial Moves

In conclusion, I would like to say that refinancing loans is a great way to control your money smartly and even save some over a period of time. Refinancing loans at lower interest rates or with better loan terms means you will lower your monthly installments and boost your income flow. The important thing is to keep informed, look at different lenders, and check that refinancing will really improve your finances. These positive refinances will keep you on the way to reaching your financial success.

This was all about refinancing loans and saving money. We hope you enjoyed reading and learned something valuable today. In case you want to learn more about the psychology of money you can read our article on that topic.