The financial world is full of valuable insights. Accordingly, there are various methods that help you manage your finances in a smart way in order to not to lose money or make wrong decisions on your way.

Nowadays, it’s more than necessary to understand basic financial tips that are useful even in everyday life. It is important to be financially literate, and understand the psychology of money.

So, our blog is here to help you to start your moneywise journey, and today’s topic is about the 3 biggest strategies for paying down debt. Here you will find out which strategy is the most relevant for you. We will help you choose the right way to pay off debt while saving your money. So, let’s get started.

The 3 Biggest Strategies for Paying Down Debt

There are many approaches you can use when eliminating debt, but financial experts agree that only 3 strategies are the most effective ones. The first strategy is the debt snowball method which concentrates on paying off the smallest balances first in order to have significant progress later. The second one is the debt avalanche method which concentrates on targeting debts with the highest rates to save the most money. And the last one is called debt consolidation. By using the third method you combine multiple debts in one payment and most often with a lower interest rate.

Strategy N1: The Debt Snowball Method

The Debt Snowball Method is one of the most well-known strategies for paying down debt. On one hand, this method is all about early wins, on the flipside, this method is not mathematically the cheapest one. For most people this method is attractive in practice because it helps people to be motivated and fully pay their debt.

We’ve selected the 5 special characteristics of the debt snowball method to help you understand it better.

- The debt snowball method mostly prioritizes debts by its balance size and not by its interest rate.

- In case of the debt snowball method you pay the smaller debts quickly and experience fast results.

- This method follows the principle of behavioral finance.

- The debt snowball method already hints that it makes a snowball effect. So, when you pay off one debt, the amount you were paying on it doesn’t appear because you roll it into the next debt.

- Lastly, the debt snowball method is simple because here you you list debts from smallest to largest.

Below, in the picture, you can see what are the 5 benefits of the debt snowball method:

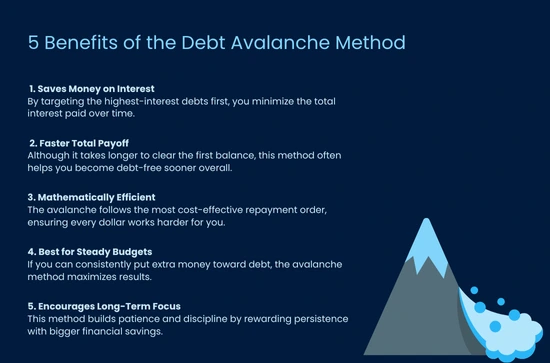

Strategy N2: The Debt Avalanche Method

The Debt Avalanche Method is another one of the most successful approaches for paying down debt. Although this method is all about saving the maximum amount of money on interest, it often takes longer to completely pay off the first debt. For disciplined people, however, the avalanche method is still attractive because it is the mathematically cheapest way to eliminate debt.

We’ve selected the 5 special characteristics of the debt avalanche method as well to help you understand it better.

- The debt avalanche method concentrates on paying debts with the highest rates first, regardless of their balance size, which helps you minimize the total interest of the debt.

- When you pay the expensive debts first, you reduce how much interest accumulates. Obviously, you will save more money compared to the debt snowball method.

- In contrast to snowball method, the avalanche approach may take longer before you completely pay off your first balance. In case you need quick results and early wins, you may need to chose the snowball method.

- Pay attention to your budget changes, because due to rising expenses your progress may slow down.

- And lastly, the avalanche method requires patience and focus because your motivation must come from knowing you are saving money on interest in the long run, not from seeing immediate progress.

And below, in the picture, see the 5 benefits of the debt avalanche method:

Strategy N3: Debt Consolidation

Debt Consolidation is another widespread strategy for paying down debt. This strategy is all about simplicity because you combine all your loans in one. Accordingly, instead of having to pay 3-5 loans monthly, you just pay only 1 loan. The principle of the debt consolidation is the following “One Big Loan Instead of Many”. Lowering the interest rate and making payments easier is the primary objective. But you should also think about the downsides, like having to pay for a longer time (which can mean paying more interest), your credit score dropping a little at first, and the fact that you’ll need to change your spending habits so you don’t fall back into debt.

We’ve also found out the 5 special characteristics of debt consolidation to help you understand it better.

- Debt Consolidation strategy combines multiple debts into one which makes repayment easier to manage.

- The goal of the debt consolidation method is to provide one loan at a lower rate.

- This method obviously simplifies your payments as you go from paying 3-5 monthly payments to just one payment each month.

- Note that you need to make regular, on-time payments because at first your credit score might drop a little. In case you make regular payments, your score can go back up and even get stronger over time.

- Finally, you need to maintain self-control in order to succeed and pay down your debt.

And below, in the picture, you’ll find 5 advantages of the debt consolidation method.

Snowball vs. Avalanche: Which Is Better?

Now that we are aware of these two strategies for paying down debt we can take a look at which one is better and suitable especially for you. Before comparing, let’s quickly remind ourselves:

- Snowball Method → Focuses on the smallest debts first for fast wins.

- Avalanche Method → Focuses on the highest-interest debts first to save more money.

Advantages of each method:

| Snowball Method | Avalanche Method |

| Builds motivation, creates momentum, and feels rewarding early on. | Saves the most money overall, reduces interest costs, and is financially efficient. |

Disadvantages of each method:

| Snowball Method | Avalanche Method |

| You might pay more in interest because you’re not tackling the most expensive debt first. | Can feel slow at the beginning, which makes it harder for some people to stay committed. |

Who benefits much from each:

| Snowball Method | Avalanche Method |

| People who need quick progress and encouragement to stay consistent. | People who are disciplined and focused on minimizing costs. |

How to Choose the Right Debt Repayment Plan

So, how do you know which debt strategy is right for you? Reading this article, one can comprehend that selecting tactics for managing debt largely depends on one’s personality and motivational factors. For those needing rapid results and wanting to feel a sense of achievement, the debt snowball method is preferred. Conversely, those who are disciplined, driven by numbers, and find motivation in the idea of reducing overall interest are better suited to the avalanche method. And, oppositely, those who prefer simplicity, get stressed by managing multiple payments, and want a single predictable bill each month the debt consolidation might be the right choice.

As you can see it is not that hard to choose the right strategy for paying down debt․ All you need to do is to be financially literate and read more relevant topics about finances, such as how to create a budget with a low income, etc.

To make your decision, start by writing down all your debts, their interest rates, and balances. Then ask yourself: “Do I value motivation or money savings more?” Once you know your answer, choosing the right plan becomes simple.

Remember, the best strategy is the one you can stay loyal to. And whichever path you take, every step brings you closer to financial independence.

Top Mistakes People Make When Paying Down Debt

It is crucial to know what mistakes people make when they pay down debt. Be aware and always remember the following rules so that you avoid making the same mistakes on your way.

- Sometimes people pay only just the minimum each month without understanding that this keeps them in debt much longer and costs more in interest. Yes, it feels easier short-term but it delays real progress.

- Most people take on new debt during the action of paying off their old debt.

- Majority of debtors ignore the interest rates of loans. They pay debts randomly or based on their convenience. Without a clear strategy, you can waste a lot of money on interest.

- In many cases, debtors don’t have an emergency fund which can save them during hard financial times, especially when surprise expenses arise.

- In many cases, people lose motivation and stop their repayment plan too early. Paying off debt takes time, and progress may feel slow at the very beginning. But if you stay consistent, every single payment brings you closer to financial independence.

Conclusion

In Summary, by following the right strategies for paying down debt, you’ll not only save money but also gain peace of mind and confidence in your financial future.

If you found this article helpful, we recommend diving deeper into your moneywise journey with these guides: